Nothing focuses a mind better than paying for profits.

Law firms that can pay at market levels enjoy the advantage of diminished partner exits and increased appeal to attorneys in weaker competitor firms. Transparency in the compensation process is also essential to maintaining partner satisfaction.

The fundamentals of market-based compensation include paying partners based on profit contributed, efficient overhead and good cash flow. As a general rule, firms that can pay partners at least 85% of their added profits are market competitive.

Building this type of data-driven compensation system may seem challenging in the beginning, but if you are committed to client/matter profitability, the actual compensation process is only a little more work.

Lastly, the process can be transformational. As law firm consultants, we have seen the direct benefits of law firm partners who are given incentives. These law firm partners are more willing to endure the short-term pressures related to change.

How do law firms pay for profitability?

For starters, a firm must develop origination splitting policies and a methodology for equating client profitability to income. Additionally, an education process is necessary to ensure that partners understand the mechanics of the system. As nothing focuses a mind like compensation, most partners will at least develop a working knowledge of the fundamentals since they determine law firm partner salary.

Origination policies:

One of the more challenging aspects of an objective law firm partner salary system relates to origination sharing. Many originations are easy to identify and can be attributed to a lawyer or group of lawyers. Split originations can be more difficult for several reasons, and we recommend publishing base-level origination guidelines.

We recognize that there are strategic, cultural, and philosophical considerations related to origination sharing. In this post, we are focusing on the issues regarding the implementation of an agreed-upon compensation system in this post.

In all cases, splitting profits is best done within the book of business and among the partners reaping the benefits. Obscuring contributions leads to a general lack of trust and can send mixed messages.

Let’s assume our sample law firm has adopted the following origination guidelines.

Sample Law Firm Origination Guidelines

The following guidelines are not rigid and have been developed using commonly occurring scenarios. Law partners are free to spit origination profits on any mutually agreeable basis. Originating partners are also free to cede profits in the form of a bonus to support partners for their efforts.

|

TYPICAL SCENARIOS |

ORIGINATION SCENARIOS |

COMMENTS |

|

|

100 % to originator |

In these situations, there is no origination sharing. |

|

Originate, work and co- manage with another partner, originator retains total relationship responsibility |

100% to originator |

Originator may share profit with co-manager for training and leverage profits. |

|

|

Origination is normally weighted in favor of the client service partner. Typically (but not always) origination splits would be: - 20% to originator- 80% to client service partner |

The originating partner brings in work and cedes relationship to another partner in the firm. An issue arises when origination sharing goes on for a longer period. In these instances, we recommend a scaled participation. For example, 20% to the originator in year 1, 10% year 2, 5 % year 3 and no sharing with originator after that. |

|

Originate and associate special expertise partner, originator also works and retains full relationship responsibility

|

Origination sharing depends on the role of the special expertise partner (SEP). Origination tilts in favor the SEP if they participate in the client or matter procurement process. Origination credit to the SEP may range from 20 to 80%. |

A typical example of this situation includes a business client that engages a firm for a contract dispute that ends up in litigation. The origination is not shared before the litigation, but shared after litigation commences. |

Originate, work and manage with total relationship responsibility

Originate, work and manage with total relationship responsibility

Originate and handoff, client service partner assumes relationship responsibility

Originate and handoff, client service partner assumes relationship responsibility

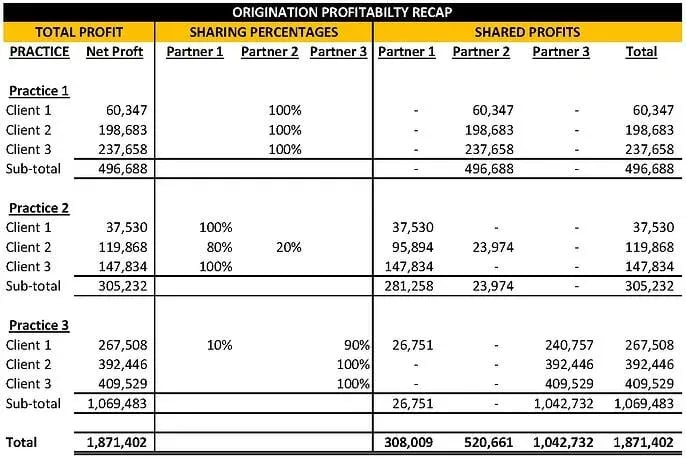

After consulting the firm’s origination guidelines and reaching a mutual agreement, the following origination and profit splits are relevant:

The remaining assumptions are as follows:

- 95% of the firm’s profit is distributed based on contributed profits

- Managing partner compensation is set at $50,000

- Other subjective bonuses are awarded based on a vote of the partners

- Unused subjective bonus dollars are returned to the profit pool

- Firm cash net income was $2,397,606

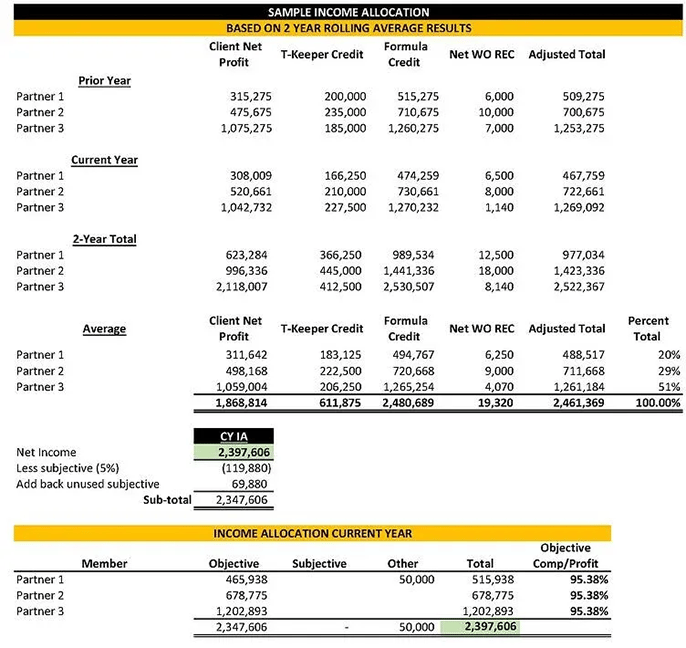

- A two-year rolling average of contributed profit is used to determine objective profit pool participation

- Prior year profit contributions for each partner are as follows:

- Partner 1: 315,275

- Partner 2: 475,675

- Partner 3: 1,075,275

- Partner timekeeper credit is considered at 35% of timekeeper billings are also subject to a two-year rolling average. Prior year timekeeper averages for each partner are as follows:

- Partner 1: 200,000

- Partner 2: 235,000

- Partner 3: 185,000

- Current/Prior year AR write-offs were as follows:

- Partner 1: 6,500/6,000

- Partner 2: 8,000/10,000

- Partner 3: 1, 140/7,000

With these data, we are able to prepare the current year’s income allocation. See the table below:

In this sample firm, all results are averaged over a two-year period and compared and rated as a percent of all client net income. Applying each partner's percent of prior two years rolling average profitability to the firm’s current year cash net income indicates current year objective compensation.

Note that partner payroll costs for compensation are removed from the client profitability analysis. In this example, there is no guaranteed pay for partners.

Our management consulting experience has shown most clients to prefer an averaging method for promoting stability. A good year will still impact current year earnings, but banking some of it to cushion against a bad year is preferred. Each firm is different, but longer averaging periods may be too slow to react to current results.

If this were an actual firm, it would be very healthy. Notice the objective compensation to profit contributed ratio. Being able to pay out 95% (95.38) of added profits is a strong performance in any market. Finally, in this example, recall that the managing partner pay is $50,000 and in the "Other" column. Unused subjective dollars increased the objective profit pool.

If this were an actual firm, it would be very healthy. Notice the objective compensation to profit contributed ratio. Being able to pay out 95% (95.38) of added profits is a strong performance in any market. Finally, in this example, recall that the managing partner pay is $50,000 and in the "Other" column. Unused subjective dollars increased the objective profit pool.